Turning 65 is not just another birthday. It is the age when many people first become eligible for Medicare, start comparing Medigap and Medicare Advantage, revisit Social Security timing, and make important retirement and estate-planning decisions. The tricky part is that these decisions do not all happen on the same day.

Some steps should begin months before your birthday. Others depend on whether you are still working, whether you have employer coverage, whether you contribute to a Health Savings Account, and whether you plan to claim Social Security now or later. Use this turning 65 checklist to organize the decisions that matter most and avoid the deadlines people commonly miss.

Why Turning 65 Requires a Plan

Age 65 is most closely associated with Medicare, but it also touches your taxes, retirement income, legal documents, and long-term care strategy. The biggest mistake is treating everything as one automatic event. Medicare may be automatic for some people who already receive Social Security or Railroad Retirement Board benefits, but many people need to sign up themselves.

It is also important to know that 65 is usually not full retirement age for Social Security. For people born in 1960 or later, full retirement age is 67. That means your Medicare timing and your Social Security claiming strategy may be two separate decisions.

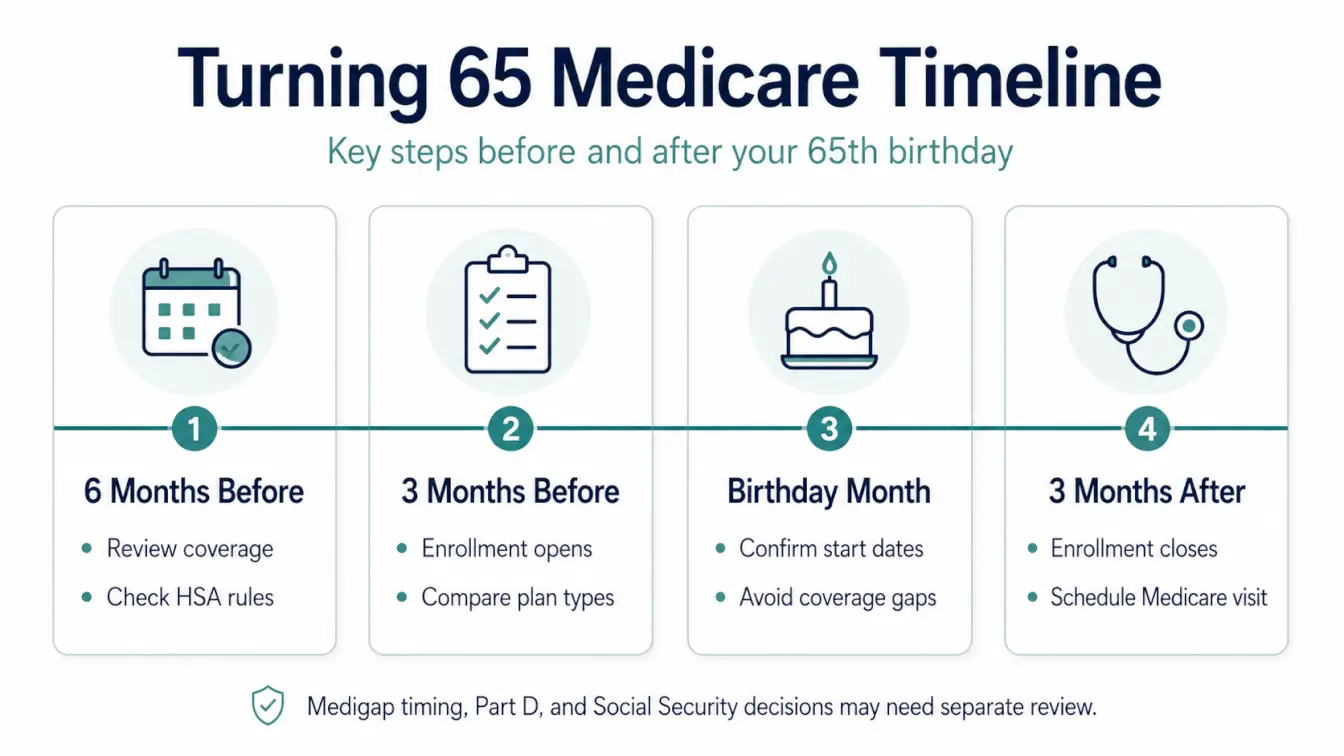

Your Turning 65 Timeline at a Glance

The exact order can vary depending on your birthday month and current coverage, but these checkpoints give you a practical way to pace the process. Use the timeline to see which decisions usually need attention before, during, and shortly after your 65th birthday month.

| When | What to Focus On |

|---|---|

| 6 months before 65 | Review current health coverage, compare Medicare paths, check HSA rules, and start retirement budget planning. |

| 3 months before 65 | Your Medicare Initial Enrollment Period generally opens. Decide whether to enroll in Parts A and B, and compare Medigap, Medicare Advantage, and Part D options. |

| Birthday month | Confirm coverage start dates, update doctors and prescriptions, and make sure there are no gaps in health insurance. |

| 3 months after 65 | Your Initial Enrollment Period generally ends. Missing it may lead to delays and late enrollment penalties unless you qualify for a Special Enrollment Period. |

| First 12 months of Part B | Schedule your one-time Welcome to Medicare preventive visit. |

Before You Compare Plans, Gather These Details

Medicare decisions become much easier when you compare plans against your real life instead of against a generic brochure. Before you shop, make one simple document with your current doctors, preferred hospitals, pharmacies, prescriptions, dosage amounts, and how often you travel outside your local area. Add any upcoming surgeries, specialist visits, expensive medications, or chronic conditions that may affect your plan choice.

Also write down the coverage you have today. Is it employer group coverage from active work, retiree coverage, COBRA, VA benefits, Marketplace coverage, Medicaid, or something else? These categories can affect whether you should enroll in Medicare at 65, whether you may delay Part B, and how your current coverage pays once Medicare begins.

Finally, choose your decision priorities. Some people want the lowest monthly premium. Others care more about provider flexibility, fewer surprise bills, nationwide access, prescription coverage, or predictable out-of-pocket costs. There is no universal answer, but there is usually a better answer for your doctors, budget, and health needs.

Quick details to gather before comparing plans:

- Current doctors, specialists, hospitals, and preferred pharmacies

- Prescription names, dosages, and refill frequency

- Current coverage type, including employer, retiree, COBRA, VA, Marketplace, Medicaid, or other coverage

- HSA status and whether you are still making contributions

- Travel habits, budget concerns, and preferred level of provider flexibility

Part 1: Medicare and Health Coverage Steps

Start with the health coverage decisions because they tend to have the most immediate deadlines. These steps help you understand when to enroll, how different Medicare paths work, and which timing issues can affect your costs later.

1. Understand your Medicare Initial Enrollment Period

For most people turning 65, the Initial Enrollment Period lasts 7 months: the 3 months before your birthday month, your birthday month, and the 3 months after. This is your first chance to sign up for Medicare Part A and Part B.

2. Decide whether you need Medicare now if you are still working

If you or your spouse has current employer group health coverage, you may be able to delay Part B without a late penalty. This depends on the type of coverage and employment situation, so ask the employer benefits administrator how Medicare will coordinate with your plan.

3. Compare Original Medicare, Medigap, and Medicare Advantage

Original Medicare includes Part A and Part B. Many people add a standalone Part D drug plan and a Medicare Supplement policy, also called Medigap, to help with out-of-pocket costs. Medicare Advantage is an alternative way to receive Medicare benefits through a private plan, often with networks and plan-specific rules.

4. Do not overlook prescription drug coverage

Even if you take few medications today, compare Part D or Medicare Advantage drug coverage. Going without creditable drug coverage can create future penalties.

5. Know your Medigap Open Enrollment window

Your one-time federal Medigap Open Enrollment Period starts the first month you are 65 or older and enrolled in Part B, and lasts 6 months. During this period, insurance companies generally cannot use medical underwriting to deny you a Medigap policy or charge more because of health problems.

Important Medigap timing note

Your Medigap Open Enrollment window is different from the annual Medicare Open Enrollment Period. Missing the protected Medigap window can matter because later applications may involve medical underwriting unless you qualify for a guaranteed issue right.

6. Handle HSA contributions carefully

Once you are enrolled in Medicare, you cannot contribute to an HSA. If you delay Medicare and apply later, premium-free Part A can be retroactive up to 6 months, so many people need to stop HSA contributions 6 months before applying for Medicare or Social Security benefits.

7. Schedule your Welcome to Medicare visit

Medicare Part B covers a one-time Welcome to Medicare preventive visit within your first 12 months of Part B. This is not a full physical, but it can help you review risk factors, preventive services, screenings, vaccines, and referrals.

Part 2: Financial and Retirement Planning

After the Medicare basics are mapped out, look at how health coverage fits into your broader retirement picture. Income timing, taxes, savings withdrawals, and monthly medical costs can all affect the plan that feels comfortable after 65.

8. Review your Social Security claiming strategy

You can claim retirement benefits as early as 62, but claiming before full retirement age usually reduces your monthly benefit. Waiting can increase the benefit, up to age 70. Before claiming, compare your income needs, health, spouse benefits, work plans, and tax situation.

9. Build a retirement income and spending plan

Turning 65 is a good time to shift from a savings-only mindset to a distribution plan. List expected income from Social Security, pensions, retirement accounts, annuities, part-time work, and other sources. Then compare that with housing, taxes, health costs, prescriptions, travel, and family support.

10. Maximize catch-up contributions if you are still working

Workers age 50 and older may be able to make catch-up contributions to retirement plans, and some people ages 60-63 have higher catch-up limits under current rules. Check the current IRS limits and your employer plan rules before the end of the year.

11. Budget for Medicare premiums and out-of-pocket costs

Many people pay no premium for Part A, but Part B has a monthly premium and an annual deductible. You may also have Medigap premiums, Medicare Advantage costs, Part D premiums, prescription copays, dental or vision costs, and income-related surcharges if your income is higher.

Part 3: Legal, Family, and Future-Care Preparation

Turning 65 is also a useful checkpoint for documents, family conversations, and future-care planning. These steps are less about a single enrollment deadline and more about making sure the right people, records, and plans are in place before they are urgently needed.

12. Update your will and beneficiary designations

Your will matters, but beneficiary forms on retirement accounts, life insurance, annuities, and bank accounts can control where assets go. Review them after major life changes, including marriage, divorce, death of a spouse, new grandchildren, or a move to another state.

13. Put powers of attorney and health care directives in place

A financial power of attorney, health care proxy, and advance directive can help trusted people act for you if you cannot make decisions. These documents are easier to complete before there is a crisis.

14. Discuss long-term care planning

Medicare does not cover most long-term custodial care. Consider whether long-term care insurance, hybrid life insurance, savings, family support, or Medicaid planning may be part of your future-care strategy.

15. Review your doctors, prescriptions, and preventive care

Before choosing a Medicare path, make a list of your doctors, hospitals, medications, pharmacies, and upcoming procedures. This helps you compare networks, drug formularies, and potential out-of-pocket costs.

Bonus step: Plan the life you want after 65

The practical checklist matters, but so does your quality of life. Think about travel, volunteering, part-time work, fitness, senior discounts, community, and where you want to live over the next 5 to 10 years.

Medigap vs Medicare Advantage: Quick Comparison

One of the biggest choices at 65 is whether you want Original Medicare with a supplement strategy or a private Medicare Advantage plan. This comparison highlights the practical differences that often matter when you look at doctors, prescriptions, travel, and expected costs.

| Question | Original Medicare + Medigap | Medicare Advantage |

|---|---|---|

| How it works | You keep Original Medicare and add a Medicare Supplement policy to help pay some out-of-pocket costs. | You get Medicare benefits through a private Medicare Advantage plan. |

| Doctor access | Generally broader access to providers who accept Medicare. | Often uses provider networks and plan service areas. |

| Prescription drugs | Usually requires a separate Part D plan. | Many plans include drug coverage, but details vary. |

| Costs | Typically has a separate Medigap premium plus Part B and Part D costs. | May have low or $0 plan premiums, but copays, coinsurance, networks, and out-of-pocket limits vary. |

| Best fit | Often preferred by people who want predictable medical costs and provider flexibility. | Often considered by people who want bundled benefits and are comfortable with plan rules. |

There is no single best choice for everyone. The right fit depends on your doctors, prescriptions, travel habits, budget, health conditions, and preference for flexibility versus bundled plan features.

Common Mistakes to Avoid When You Turn 65

Most Medicare mistakes happen because people assume one rule applies to every situation. Before you choose coverage or delay enrollment, watch for these common issues that can create penalties, gaps, or fewer plan options later.

- Assuming Medicare starts automatically when it does not.

- Missing the Initial Enrollment Period because you thought 65 was only about Social Security.

- Keeping HSA contributions after Medicare enrollment begins.

- Choosing a plan without checking doctors, hospitals, prescriptions, and pharmacies.

- Confusing the annual Medicare Open Enrollment Period with the one-time Medigap Open Enrollment Period.

- Assuming COBRA or retiree coverage gives the same protection as current employer group coverage for delaying Medicare.

- Waiting until a health issue appears before comparing Medigap options.

What to Do Next

If you are turning 65 soon, start with the basics: write down your birthday month, current insurance type, employer coverage status, HSA status, doctors, prescriptions, and preferred hospitals. Then compare your Medicare options before your enrollment window closes.

A smoother Medicare start begins with a clear checklist

A licensed Medicare advisor can help you compare Original Medicare with Medigap, Medicare Advantage, and Part D drug coverage based on your actual needs. MedigapRx helps people understand the tradeoffs clearly so they can move into Medicare with fewer surprises and more confidence.

Frequently Asked Questions

These common questions cover the Medicare and retirement timing issues that often come up as people approach 65. Use them as a quick final check before making enrollment or planning decisions.

Do I automatically get Medicare when I turn 65?

Some people are enrolled automatically, usually because they are already receiving Social Security or Railroad Retirement Board benefits before 65. If you are not receiving those benefits, you generally need to sign up for Medicare yourself.

What happens if I miss my Medicare Initial Enrollment Period?

If you miss your Initial Enrollment Period and do not qualify for a Special Enrollment Period, you may have to wait to enroll and may pay late enrollment penalties for as long as you have certain Medicare coverage.

Should I sign up for Medicare if I am still working at 65?

It depends on whether you or your spouse has current employer group health coverage and how that coverage coordinates with Medicare. Ask the employer benefits administrator before delaying Part B.

When should I buy a Medigap policy?

The best-known protected window is your one-time Medigap Open Enrollment Period, which begins when you are 65 or older and enrolled in Part B. It lasts 6 months.

Can I keep contributing to an HSA after I enroll in Medicare?

No. Once enrolled in Medicare, you cannot contribute to an HSA. If you delay Medicare and apply later, Part A may be retroactive up to 6 months, so plan HSA contributions carefully.

Is 65 my full retirement age for Social Security?

For most people turning 65 now, no. Full retirement age depends on birth year. For people born in 1960 or later, full retirement age is 67.